A Fallen Angel

This week we discuss Adyen, Japan's shocking demographics, and disruption in vertical software

Dear Clients and Friends of Farrer 36, we are pleased to bring you the Farrer 36 Blog, which includes our latest posts, data, and general articles/videos we find interesting. Happy reading and happy investing!

Disclaimer - This newsletter is for informational purposes only. None of the below should be considered investment advice nor solicitation for investment. Please see full disclosures at the end of this newsletter.

Latest Blog Post

A Fallen Angel

Adyen reported earnings last week, and the market responded by eviscerating the stock, reducing the market cap by ~20%. I’ve been invested in the company in the past and have been an admirer of the business and management for quite a while, so I decided to refresh my thinking on the company.

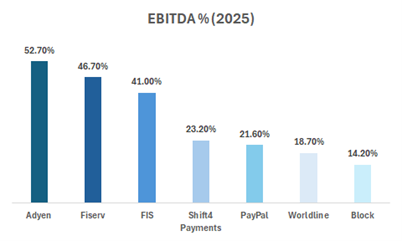

For those unfamiliar, Adyen is a leader in the payments space, processing payments for enterprise customers such as Uber, McDonald’s, and Spotify. Adyen is one of the most unique companies in the payments space for a few reasons: their extreme aversion to M&A, their unified commerce model (for example, whether you shop at Nike’s stores or online, Adyen is processing your credit card), and for having a management team known for thinking long-term. Furthermore, it has an enviable financial profile, with EBITDA margins of ~53% and topline growth compounding at nearly 30% over the past six years.

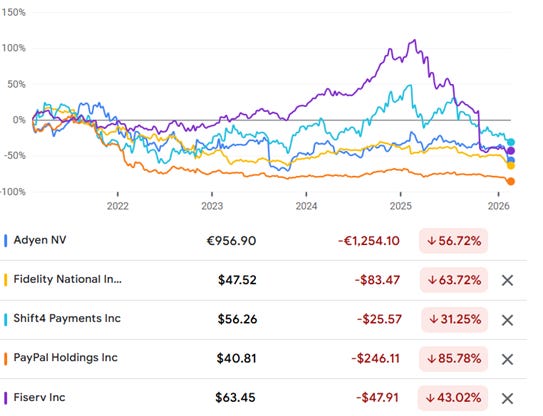

Despite all the above – Adyen has seen a heavy de-rating of its valuation.

Granted, 120x EBITDA in 2021 was too high a valuation, but is the current valuation too low for a company with the financial metrics I mentioned earlier?

To answer that question I believe there is significant value in Stanley Druckenmiller’s strategy of looking at the industry or sector first, and then the stock. Payment stocks, broadly speaking, have had a tough time over the past five years.

There are a few reasons for this:

The simplest answer is that valuations got too hot coming off COVID. I’m in the camp that thinks that very few (and I mean fewer than you can count on two hands) businesses deserve to trade at over 25–30x P/E for an extended period. You really need some unassailable advantage, longevity, and constant execution. Few companies fit this bill — maybe Costco, maybe Microsoft or Apple, but that’s about it. This is especially true in a world where the tech landscape is changing so fast. As you’ll see below, competition in the payments space is not conducive to elevated long-term valuations. In hindsight, PayPal trading at 45x forward EV/EBITDA in 2021 was ludicrous.

Race to the bottom: The more I study this industry, the more I believe payments is a race to the bottom with regard to take rates. This is based on conversations with customers, the use of orchestration layers, and competition. We have seen Adyen’s take rates (the amount they receive on each transaction processed) drop from 0.21% in 2021 to about 0.17% this year. My initial defense of Adyen was that this was fine — in many ways, this is part of their core strategy (higher volumes lead to a discount on price). Considering their margins, Adyen has the lowest cost to serve, and thus, as take rates fall, they would be in the best position to take business from competitors that cannot compete. I think that still remains true — but I wonder if it’s enough. I believe the market wants to see payment companies (and finance companies in general) monetize across more surface area. Just doing bread-and-butter payment processing or transfers is no longer cutting it. Say what you want about Robinhood, but their pace of execution and rollout of new products/features is just insane. To its credit, Adyen is strengthening its product beyond just processing. Unified Commerce, Platform (loans, cash-out, issuing, etc.), Dynamic Identification, etc., are all value adds. I’m still unsure how this is reflected in the financials or even if we can attribute certain features that way — but I do think Adyen has gotten the message.

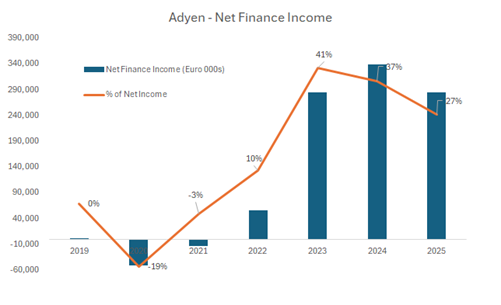

This is a transitory effect, but as interest rates decline, pressure will be put on EPS. Most payment companies enjoy float from customer flows (even if it’s for a short time); thus, other income lines were bloated over the past few years. For example, in 2023, net finance income made up 41% of Adyen’s net income. The issue with this is that you have a bifurcation of EBITDA and EPS growth — and this does not screen well.

Competition — every quarter I hear about a new payments company getting funded by VCs, and this is just in my neck of the woods. There always seems to be some gap in the market, some new geography, or some new infrastructure (stablecoins) that attracts venture funding.

On the plus side for Adyen, all these companies eventually must become profitable — so they can’t keep burning cash and lowering take rates forever. But on the downside, stablecoins might allow competitors to spin up faster, and what Adyen has taken years to build could be built much more quickly. More importantly, part of Adyen’s business is quite commoditized. As a refresher, Adyen reports in three segments: Digital, Platforms, and Unified Commerce. Digital makes up 51% of volumes and about 55% of revenues. Digital is the most basic of Adyen’s offerings, essentially processing online payments. Volume growth has come down from 40% in H2 2022 to -1% this past half. Much of this is driven by a slowdown in a large customer (Cash App, I believe), but even accounting for Cash App, growth in this segment was just 11%. I remember in mid-2023 Adyen’s stock fell some 60% because of slower volume growth at a time when PayPal’s Braintree became extremely aggressive in the Digital vertical. My point here is simple: this constant competitive dynamic does limit long-term returns in the industry and threatens terminal value. This is what gets missed in the software conversation — it’s not so much that corporates will vibe-code their own critical software; it’s that the competitive set will grow significantly. (As a quick aside Shift4 founder Jared Isaacman made an interesting argument that each major payments company is operating in its own niche - which is sort of true - but for how long will that remain so?)

Now moving on to Adyen specifically – I do think there is a bear case that’s worth spending some time on. It’s been presented by my friend Ali, you can read his thread here.

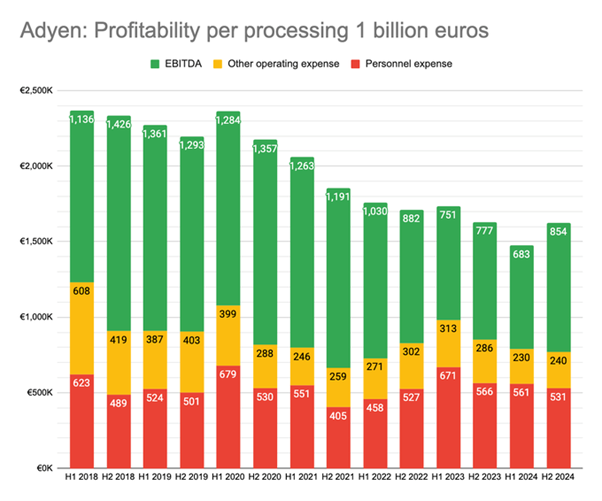

But the gist of the bear case is that Adyen was earning less profit for each additional euro processed. This was driven by the fact that Adyen went on a bit of a hiring spree over the last three years, more than doubling its employee count since 2021. This led to depressed margins, with EBITDA margins falling to 46% in 2023. However, in 2025 we did start to see Adyen increase profit per euro processed — implying efficiencies. Furthermore, the company thinks it can reach 55% margins within the next few years. That said, Adyen has indicated they will continue to invest in the business and are looking to hire even more in 2026 — so the metric should be watched — but for now, this overhang is gone.

All the above is backward-looking — investing is a game of predicting the future. Which brings us to the most recent earnings, which were not well received by the market. The issues here were:

A guidance reduction from 20–25% growth to 20–22%. The midpoint moved from about 22.5% to 21% — not huge, but in a market that expects perfection, it was more than the stock could take.

Digital volumes still struggling to grow due to the “one large customer.” However, considering that H1 showed a decline of 9% and H2 showed a decline of 1%, it does seem 2026 will show growth as the Digital vertical laps tough comps. Although, based on the above discussion of competitive dynamics, I do think that investors should keep expectations of significant growth in this vertical low.

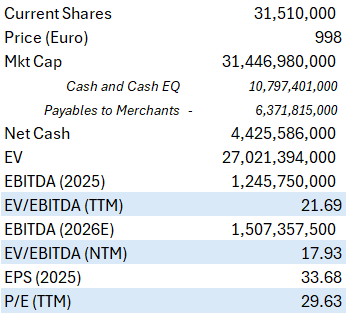

Cash hoard — Adyen holds about €4.4bn in cash (be careful how you calculate Adyen’s cash — much of what’s reported on their balance sheet is not “theirs”). Investors are wondering what they are going to do with it. Adyen doesn’t do any M&A, throws off free cash flow, and does not pay a dividend. So I guess the solution is buybacks? It seems that management is hesitant here. In their defense I’m not sure buybacks will make that much difference considering the stock still trades at a 30x trailing P/E — but I can understand how capital allocation is a bone of contention for investors.

Personally, I thought earnings were decent — although I do understand the market’s frustration with the own goal Adyen management made by changing guidance issued just months back. It was not clear to me exactly where the conservatism came from, but it did seem that Adyen’s customers are not as bullish about their businesses as they were a few months ago, so perhaps there is some sandbagging here.

But as readers will know, I am both terrible at and uninterested in predicting the short term. With the long-term in view, the earnings call brought up two aspects of Adyen’s business that will put them in a solid position going forward volume wise and could bolster/augment take rates:

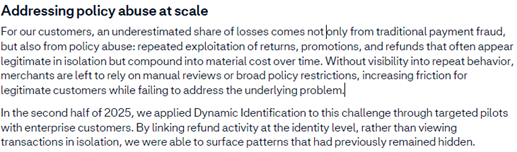

Unified Commerce: This remains one of the most distinctive parts of Adyen’s business, and one that few, if any, competitors can fully replicate. For the uninitiated, Unified Commerce (34% of total volumes) refers to merchants using Adyen for both point of sale (in-store) and online payments through a single platform. The value proposition is clear: merchants can track and understand customer behavior across channels in a unified way. Over time, this should leave Adyen sitting on a meaningful trove of transaction data — potentially digital gold in the AI age. In H2 2025, Unified Commerce volumes grew 30%, the number of multi-channel customers rose to 467 (+50), and Adyen landed Starbucks in Europe.

Their agentic commerce strategy seems sound — in a world where AI is not fully trusted, agents will be even less so. Thus, Adyen has launched a product (Dynamic Identification) that allows identification of the end customer at the identity level rather than the transaction level. This, in my opinion, should significantly increase Adyen’s value prop to customers. As the company explained —

Summarizing my thoughts above boils down to three statements:

The payments industry probably deserved its derating from the 2021 highs.

Competition, both from existing payment processors and new entrants, will continue.

Adyen is likely the best of the bunch — and still boasts enviable growth rates and profitability. Furthermore, Adyen exhibits several product and cultural traits that will likely allow it to continue to lead the pack going forward.

All that considered, the question becomes: is this the right time to buy Adyen’s stock? While I will stay away from definitive answers, it’s first worth valuing the company (price as of the 19 Feb close).

The first question worth answering is whether we should be looking at an EV/EBITDA or P/E ratio. It’s an interesting thought exercise — eventually P/E matters most (as Amazon shareholders are finding out), but for asset-light companies like Adyen, EV/EBITDA is a fine enough metric to use (especially in the short term). In that case, we are looking at one of the lowest multiples Adyen has ever traded at. The next question becomes: is it cheap enough given my three declarations above?

If you are a valuation purist, then the P/E does not look very attractive — and given that EPS will grow slower than EBITDA (due to lower interest income), the PEG is probably around ~1.65, which is nothing to get too excited about.

Two exercises worth thinking through are as follows:

What do you pay for an industry leader that has a significant edge but operates in an industry rife with competition/disruption?

What is your margin of safety in a market that seems to require perfection for high valuations?

I suspect how one answers those two questions will largely shape their view on Adyen’s stock.

Thanks for reading the above, and happy investing!

Chart of the Month

The Japanese Conundrum - The Japanese stock market might be ripping, but its demographics are falling apart. (source: Torsten Slok, Apollo)

Links of the Month

This is the best thing you will read all month - Vertical Software, are we cooked?

Wealth is what you have minus what you want - an excellent podcast about wealth featuring Morgan Housel

The DoorDash Problem - this episode of Decoder tackles how AI browsers/agents will impact ecommerce.

A fascinating tweet about the history of newspaper stocks and how it might draw parallels to software.

In case you didn’t get enough of Adyen - here is a post that paints the bull case.

A kind request - if you enjoyed this newsletter, I would be most grateful if you could give it a ‘like’ or share it. Thank you!