Truly Long-Term....

This week we discuss long-term strategies, SaaS's GFC, and an investor's last remaining edge

Dear Clients and Friends of Farrer 36, we are pleased to bring you the Farrer 36 Blog, which includes our latest posts, data, and general articles/videos we find interesting. Happy reading and happy investing!

Disclaimer - This newsletter is for informational purposes only. None of the below should be considered investment advice nor solicitation for investment. Please see full disclosures at the end of this newsletter.

Latest Blog Post

Truly Long-Term…

A few weeks ago, I was on an Emirates flight on the way back home from RV Capital’s annual meeting. I noticed the cabin crew taking Polaroids of the children on the flight and handing the photos to them in an Emirates frame. This is a genius move. There is a good chance that the child puts that photo up on a windowsill or shelf, reminding them of that wonderful holiday — and the airline that made it happen. Which carrier do you think that child will be loyal to once they grow up?

This loyalty strategy requires truly long-term thinking. Payback won’t be likely for a decade or more. It got me reflecting on other examples of long-term thinking in the world:

Adyen (a Dutch payment processor) is unique in its space. It does zero acquisitions. It prefers to build its platform from the ground up. No amalgamations, no stitching platforms together, no legacy code. It’s painstaking work and makes expanding into new countries a drawn-out affair, but Adyen has one of the most reliable and efficient platforms in the market.

Ferrari will always deliver one car less than the market demands. It makes would-be buyers wait — and wait a long time, sometimes over three years — to get their hands on a new unit. This flies in the face of conventional customer experience wisdom, but the wait is part of the long-term strategy.

Ronald James Read was an American philanthropist, investor, janitor, and gas station attendant. He was a simple man, lived frugally, and invested the money he earned over 25 years as a gas station attendant and mechanic. He held several blue-chip companies for decades and reinvested his dividends. Over time, he amassed a fortune of $8 million — most of which he gave away.

Writer Robert Caro is famous for his work on Lyndon Johnson. However, the first book on the topic required extreme research: hours in presidential libraries, dozens of interviews with family and friends, and even relocating his family to where Johnson grew up (the backwaters of Texas) to better understand the man. All in all, it took nearly a decade for Caro to finish the first volume on the life of the U.S. president.

Steve Ballmer has held on to most of his Microsoft shares since 1980. It took over 40 years, but now he makes nearly $1 billion a year just in dividends.

Sushi chef apprentices in Japan train for 3–8 years working only on rice. It’s believed this is the minimum time needed for someone starting from scratch. During this period, they are also observing, asking questions, and learning about all parts of the business. Only several years later do they put all that accumulated knowledge to work.

Another example from Japan: large manufacturers maintain very long-term relationships with their suppliers. It’s not about getting the lowest price; it’s about reliability, shared learning, and resilience during downturns. My favourite story here is from Kotobuki Spirits (Japan’s See’s Candies). During COVID, Kotobuki needed a new ice-pack supplier because of longer inventory cycles. One supplier agreed to do business but admitted they would operate at a loss. Kotobuki refused to accept this and instead worked with the supplier to reduce their costs. The deal ended up being economical for all sides. (source)

There are also several companies that have remained intensely consistent over decades despite market pressure. Berkshire Hathaway has never paid a dividend during the Buffett era (over 60 years). Coca-Cola didn’t change its recipe for decades until the “New Coke” misstep in 1985. Costco has capped its gross margins for decades in order to win on price. Hermès has resisted scaling production even as demand has exploded — artisans train for years and hand-make most products.

Excellence takes decades, but even good results take years. It reminds me of a Bezos quote about being congratulated on strong earnings:

“When I have a good quarterly conference call with Wall Street, people will stop me and say, ‘Congratulations on your quarter,’ and I say, ‘Thank you,’ but what I’m really thinking is that quarter was baked three years ago.”

This is from a leader who understands reaping the fields years after the first seeds were planted. Many of the examples above share a common feature: the costs are obvious immediately, but the benefits are invisible for years. To outsiders, they often look inefficient (many luxury houses mass-manufacture their products), indulgent (Ferrari charges you to come pick up your own car), or even reckless at the time (Bill Gates sold much of his Microsoft stock to diversify and give to charity).

I’ve been thinking about this concept as we go into tech earnings - a moment when markets are forced to judge long-term investments using short-term scorecards. The big question on investors’ minds is how much capex will be spent this year — and whether it will be worth it. Meta has already answered: $125bn (midpoint) to be spent in 2026. The ramped-up capex spend ($72bn in 2025) is showing improving ROC, but as the absolute amount of capex rises, it remains to be seen whether each incremental dollar is spent wisely.

For each of the large tech companies, AI presents both the largest opportunity and the largest risk they have witnessed in a long while. As Google’s Sergey Brin once claimed, “I’d rather go bankrupt than lose the AI race.” Such large investments require long-term — and sometimes irrational — thinking. Time will tell.

Thanks for reading, and happy investing!

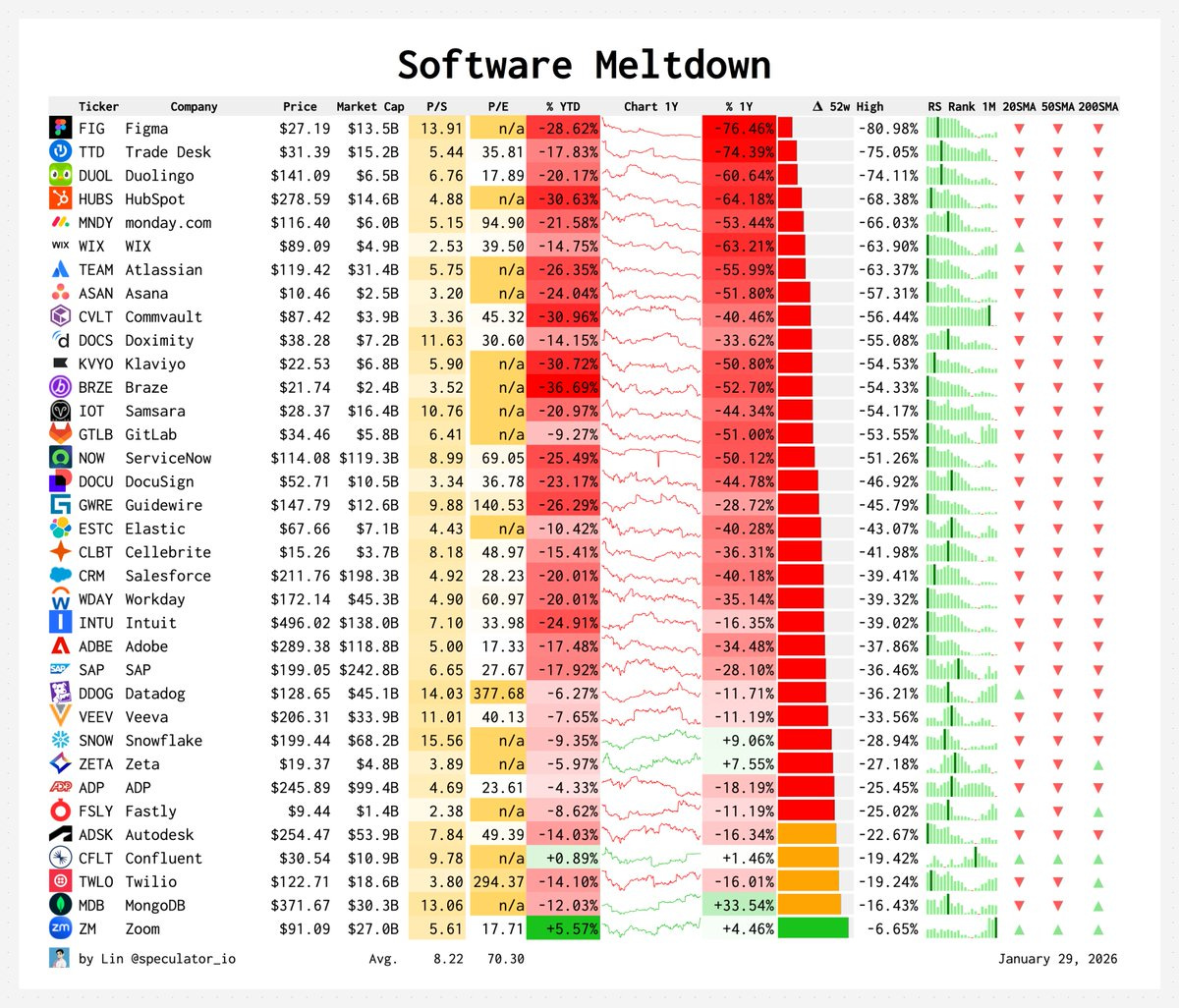

Chart of the Week

Software’s Great Financial Crisis - It’s been brutal for software investors over the past several months. The AI disruption narrative is in the driver’s seat with the accelerator slammed to the floor. (source)

Links of the Week

The last human edge - in an era of AI, a real life example on how investors can stand out.

The short case for Nvidia's stock.

We’ve covered Intellego’s fraud previously on this blog - but the forensic audit results are even more shocking than I imagined - 99% of 2025 revenues were made up!

A few things Morgan Housel is pretty sure about. A needed read in a crazy world.

A kind request - if you enjoyed this newsletter, I would be most grateful if you could give it a ‘like’ or share it. Thank you!

Brilliant, what if more public services, like education, adopted this truly long term, community-building approach instead of chasing short-term metrics?